Hm.. mintha a britekkel voltak szövetségben a második VH előtt is. jól meg is segítettek őket...Putyin ellen ukrán-lengyel-brit szövetség jön létre

https://www-novinky-cz.translate.go...tr_sl=cs&_x_tr_tl=hu&_x_tr_hl=sk&_x_tr_pto=sc

[BIZTPOL] Oroszország (a Szovjetunió utódállama)

- Téma indítója Montezuma

- Indítva

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Néztem, de nem kaptam el elejétől.Nézte legalább valaki?

Lényeg hogy menni fog a business, bővítés is lesz, közös vállalat stb. De azért elég borús volt a hangulat. Nem tudom hogy el kellet e játszani hogy gondterheltek, vagy tényleg azok. Ukrajnáról nem igen született döntés, de a kisebbségekről(így a magyarról is beszéltek. Arra lettem volna kíváncsi személyesen miket mondtak)

az 1milliárd plussz gázról áprilisben lesz döntés, vagy nem") ,ezt nem lehet félre érteni!

,ezt nem lehet félre érteni!

,ezt nem lehet félre érteni!BIDEN fő szarkeverő

Biden elnök és Zelenszkij ukrán elnök telefonbeszélgetése „nem ment jól” – írja a CNN: míg „Biden arra figyelmeztetett, hogy februárban gyakorlatilag biztos az orosz invázió, amikor a fagyos talaj lehetővé teszi a tankok áthaladását”, Zelenszkij kérte Bident, hogy csökkentse hangnemét, azzal érvelve, hogy az orosz fenyegetés még mindig kétértelmű. Mivel maga az ukrán elnök is óvatosabb álláspontot képvisel, az ukrán fegyveres erők a Donbászban, Donyeck és Luganszk orosz lakosság által lakott területe közelében tömegesen vonulnak fel.

Az EBESZ ukrajnai Különleges Megfigyelő Missziójának jelentései szerint – amelyet csak az orosz bevetésről beszélő fősodorunk eltakar – az ukrán hadsereg és a nemzeti gárda mintegy 150 ezer fős egységei helyezkednek el itt. Az USA–NATO katonai tanácsadók és oktatók fegyverkezik és képezik ki őket, és így hatékonyan irányítják őket.

Az Egyesült Államok Kongresszusi Kutatási Szolgálata szerint 1991 és 2014 között az Egyesült Államok 4 milliárd dolláros katonai segítséget nyújtott Ukrajnának, amelyhez 2014 után több mint 2,5 milliárd dollárral bővült, plusz egy milliárddal a NATO vagyonkezelői alapja, amelyben Olaszország is részt vesz. . Ez csak egy része a nagy NATO-hatalmak által Ukrajnában végrehajtott katonai beruházásoknak. Nagy-Britannia például különféle katonai megállapodásokat kötött Kijevvel, többek között 1,7 milliárd fontot fektetve Ukrajna haditengerészeti képességeinek erősítésére: ez a program az ukrán hajók brit rakétákkal való felfegyverzését, 8 gyorsrakétakilövő közös gyártását írja elő, haditengerészeti bázisok építése a Fekete-tengeren, valamint az Azovi-tengeren Ukrajna, Krím és Oroszország között. Ennek keretében az ukrán katonai kiadások, amelyek 2014-ben a GDP 3%-ának feleltek meg, 2022-ben 6%-ra nőttek, ami több mint 11 milliárd dollárnak felel meg.

Az ukrán porhordó és a biztosíték

Az USA-NATO ukrajnai katonai beruházásain kívül a 10 milliárd dolláros tervet hajtja végre Erik Prince, a Blackwater nevű amerikai katonai magáncég alapítója. titkos műveletekért (beleértve a kínzásokat és a merényleteket is), dollármilliárdokat keresve. Erik Prince terve, amelyet a Time magazin nyomozása feltárt, egy magánhadsereg létrehozása Ukrajnában a Lancaster 6 cég, amellyel Prince zsoldosokat szállított a Közel-Keleten és Afrikában, és a fő ukrán hírszerzési hivatal, amelyet az Egyesült Királyság irányít. CIA. Azt persze nem tudni, hogy mik lennének a feladatai a Blackwater alapítója által Ukrajnában minden bizonnyal a CIA finanszírozásával létrehozott magánhadseregnek. Arra azonban számítani lehet, hogy ukrajnai bázisáról titkos műveleteket hajtana végre Európában, Oroszországban és más régiókban.

Ennek fényében különösen riasztó, hogy Sojgu orosz védelmi miniszter elítélte, hogy a donyecki régióban „amerikai katonai magáncégek ismeretlen vegyszerek felhasználásával provokációra készülnek”. Ez lehet az a szikra, amely egy háború kirobbanását Európa szívében: vegyi támadást hajtanak végre ukrán civilek ellen Donbászban, amelyet azonnal a donyecki és luganszki oroszoknak tulajdonítanak, és amelyet a már korábban telepített, túlsúlyban lévő ukrán erők támadnak meg. régióban, hogy rákényszerítsék Oroszországot, hogy katonailag avatkozzon be védelmükben.

Az első vonalban, készen arra, hogy lemészárolja az oroszokat a Donbászban, az Azov zászlóalj áll, amelyet az Egyesült Államok és a NATO által kiképzett és felfegyverzett különleges erők ezredévé léptek elő, és amely kitűnik az ukrajnai orosz lakosság elleni támadásokban. Az SS Das Reich zászlaja alatt Európa-szerte neonácikat toborzó Azov parancsnoka az ezredessé előléptetett alapítója, Andrej Biletszkij. Ez nemcsak katonai egység, hanem ideológiai és politikai mozgalom is, amelynek Biletsky karizmatikus vezetője, különösen az oroszok gyűlöletére nevelt ifjúsági szervezetnek „A fehér Führer szavai” című könyvével.

Biden elnök és Zelenszkij ukrán elnök telefonbeszélgetése „nem ment jól” – írja a CNN: míg „Biden arra figyelmeztetett, hogy februárban gyakorlatilag biztos az orosz invázió, amikor a fagyos talaj lehetővé teszi a tankok áthaladását”, Zelenszkij kérte Bident, hogy csökkentse hangnemét, azzal érvelve, hogy az orosz fenyegetés még mindig kétértelmű. Mivel maga az ukrán elnök is óvatosabb álláspontot képvisel, az ukrán fegyveres erők a Donbászban, Donyeck és Luganszk orosz lakosság által lakott területe közelében tömegesen vonulnak fel.

Az EBESZ ukrajnai Különleges Megfigyelő Missziójának jelentései szerint – amelyet csak az orosz bevetésről beszélő fősodorunk eltakar – az ukrán hadsereg és a nemzeti gárda mintegy 150 ezer fős egységei helyezkednek el itt. Az USA–NATO katonai tanácsadók és oktatók fegyverkezik és képezik ki őket, és így hatékonyan irányítják őket.

Az Egyesült Államok Kongresszusi Kutatási Szolgálata szerint 1991 és 2014 között az Egyesült Államok 4 milliárd dolláros katonai segítséget nyújtott Ukrajnának, amelyhez 2014 után több mint 2,5 milliárd dollárral bővült, plusz egy milliárddal a NATO vagyonkezelői alapja, amelyben Olaszország is részt vesz. . Ez csak egy része a nagy NATO-hatalmak által Ukrajnában végrehajtott katonai beruházásoknak. Nagy-Britannia például különféle katonai megállapodásokat kötött Kijevvel, többek között 1,7 milliárd fontot fektetve Ukrajna haditengerészeti képességeinek erősítésére: ez a program az ukrán hajók brit rakétákkal való felfegyverzését, 8 gyorsrakétakilövő közös gyártását írja elő, haditengerészeti bázisok építése a Fekete-tengeren, valamint az Azovi-tengeren Ukrajna, Krím és Oroszország között. Ennek keretében az ukrán katonai kiadások, amelyek 2014-ben a GDP 3%-ának feleltek meg, 2022-ben 6%-ra nőttek, ami több mint 11 milliárd dollárnak felel meg.

Az ukrán porhordó és a biztosíték

Az USA-NATO ukrajnai katonai beruházásain kívül a 10 milliárd dolláros tervet hajtja végre Erik Prince, a Blackwater nevű amerikai katonai magáncég alapítója. titkos műveletekért (beleértve a kínzásokat és a merényleteket is), dollármilliárdokat keresve. Erik Prince terve, amelyet a Time magazin nyomozása feltárt, egy magánhadsereg létrehozása Ukrajnában a Lancaster 6 cég, amellyel Prince zsoldosokat szállított a Közel-Keleten és Afrikában, és a fő ukrán hírszerzési hivatal, amelyet az Egyesült Királyság irányít. CIA. Azt persze nem tudni, hogy mik lennének a feladatai a Blackwater alapítója által Ukrajnában minden bizonnyal a CIA finanszírozásával létrehozott magánhadseregnek. Arra azonban számítani lehet, hogy ukrajnai bázisáról titkos műveleteket hajtana végre Európában, Oroszországban és más régiókban.

Ennek fényében különösen riasztó, hogy Sojgu orosz védelmi miniszter elítélte, hogy a donyecki régióban „amerikai katonai magáncégek ismeretlen vegyszerek felhasználásával provokációra készülnek”. Ez lehet az a szikra, amely egy háború kirobbanását Európa szívében: vegyi támadást hajtanak végre ukrán civilek ellen Donbászban, amelyet azonnal a donyecki és luganszki oroszoknak tulajdonítanak, és amelyet a már korábban telepített, túlsúlyban lévő ukrán erők támadnak meg. régióban, hogy rákényszerítsék Oroszországot, hogy katonailag avatkozzon be védelmükben.

Az első vonalban, készen arra, hogy lemészárolja az oroszokat a Donbászban, az Azov zászlóalj áll, amelyet az Egyesült Államok és a NATO által kiképzett és felfegyverzett különleges erők ezredévé léptek elő, és amely kitűnik az ukrajnai orosz lakosság elleni támadásokban. Az SS Das Reich zászlaja alatt Európa-szerte neonácikat toborzó Azov parancsnoka az ezredessé előléptetett alapítója, Andrej Biletszkij. Ez nemcsak katonai egység, hanem ideológiai és politikai mozgalom is, amelynek Biletsky karizmatikus vezetője, különösen az oroszok gyűlöletére nevelt ifjúsági szervezetnek „A fehér Führer szavai” című könyvével.

150 kommentelőből 145 küldte vissza Fegyőrt a szobájába gondolkodni.A román-francia tudomisén most már milyen ügynökkel újabb hülységet mondattak a gazdái:

Fekete-Győr András nemzetbiztonsági szakértő: Magyarország fegyverezze fel Ukrajnát!

PestiSrácok.hu oknyomozó hírportál. Kell még valamit mondanom, Ildikó?pestisracok.hu

Én igen. Illetve hallgattam inkább.Nézte legalább valaki?

Ukraine's Security Chief: Kyiv Shouldn't Be Forced to Fulfill Minsk Agreements - News From Antiwar.com

The agreements require Ukraine to give autonomy to Donbas

news.antiwar.com

news.antiwar.com

Szerintem egy népszavazással ellehetne dönteni mindent de sajna ettől félnek ők is csakhogy nem az ő előnyükre

Az orosz - magyar vegyesvállalat megvolt? Orbán: "a határainkon.. az ukrán - magyar határon" véletlen elszólásNéztem, de nem kaptam el elejétől.

Lényeg hogy menni fog a business, bővítés is lesz, közös vállalat stb. De azért elég borús volt a hangulat. Nem tudom hogy el kellet e játszani hogy gondterheltek, vagy tényleg azok. Ukrajnáról nem igen született döntés, de a kisebbségekről(így a magyarról is beszéltek. Arra lettem volna kíváncsi személyesen miket mondtak)

Erről sajnos lemaradtamAz orosz - magyar vegyesvállalat megvolt? Orbán: "a határainkon.. az ukrán - magyar határon" véletlen elszólás

vissza kell majd nézzem

vissza kell majd nézzem

This article is the second of two parts about Russia’s radical new gambit in its relationship with Western powers. In part 1 I covered the recent history of the conflict, its broader historical context as well as its economic underpinnings. This part discusses Russia’s likely response to the US/NATO failure to respond to her security concerns. The video version, which covers both parts is available at this link.

Clearly, the conflict between east and west is not over ideology or a bit of territory. It is about hegemony over resource rich regions of the world and this makes the two sides’ positions intractable. The Russians clearly understand this which may explain why they presented the Western powers with a set of demands so tough that they certainly knew they would be rejected. It seems that Russia really does intend to respond with military technical measures that will jeopardize western powers’ security. So far however, even among the Russian analysts, nobody seems to know what’s coming next.

Most of the experts and officials in the West seem convinced that Russia will invade Ukraine, but I don’t think this will happen. The media also made much of Russia’s deputy foreign minister’s remarks that they don’t exclude deploying military assets in Cuba or Venezuela, which can’t be excluded longer term. A few analysts including Scott Ritter suggested that Russians might deploy medium-short range missiles targeting European capitals with nuclear capable warheads.

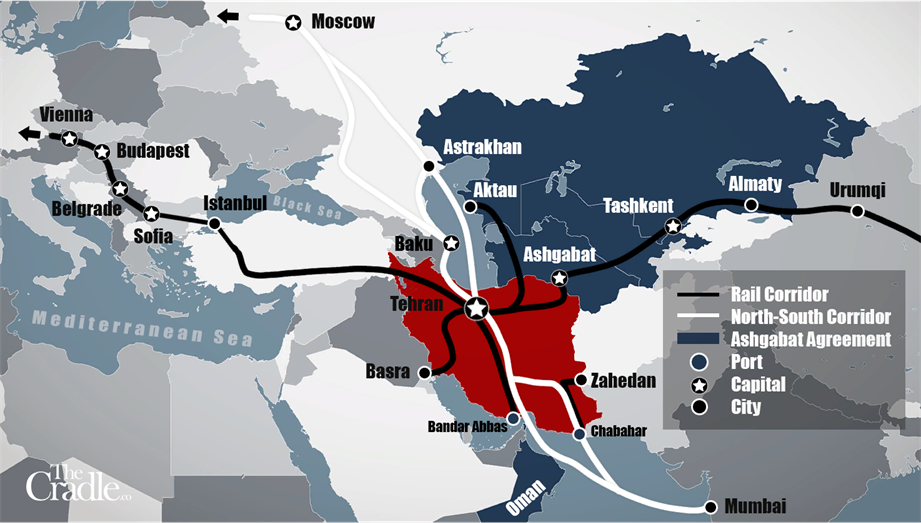

The Kremlin will probably increase pressure on the US and NATO countries in multiple ways, but my own hunch is that their first focus will be on the Persian Gulf region which is strategically of huge importance to the West but where US positions are increasingly fragile. Russia could jeopardize western power’s security in that region by implementing “military technical measures” in support of friendly regimes, primarily Iran. It is clear that Iran is becoming an important component of China’s One Belt One Road agenda and that it is being set up as the cornerstone of their security architecture in the Middle East and the Persian Gulf. These developments also have the full support from Russia.

On 27 March last year, Iran signed a comprehensive 25-year cooperation plan with China which includes cultural, diplomatic, economic and military cooperation. On 17 September Iran became a member of the Shanghai Cooperation Organization (SCO). Iran has also signed various security agreements with Russia and is in the process of negotiating a 20-year cooperation agreement modeled on the Iran-China agreement.

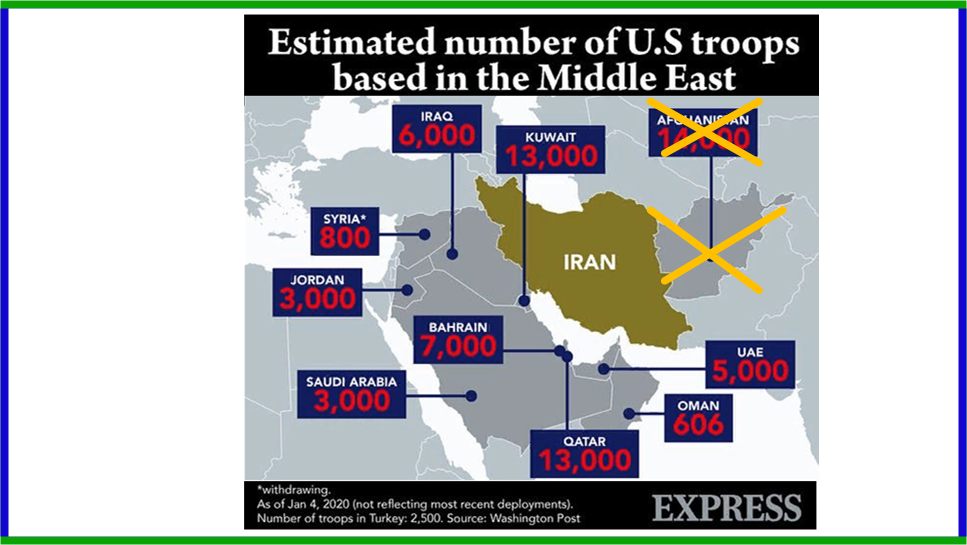

On 11 December 2021, Iranian foreign ministry spokesman Saeed Khatibzadeh stated that, “Like the 25-year cooperation roadmap we developed with China, we can do the same with major neighboring countries.” Clearly, the Iranians, who have pledged to throw the United States out of the region, have been increasingly confident in asserting their regional influence. Of course, the greatest challenge to Iran’s regional policy and security is the presence of American troops and military bases surrounding Iran as this map shows. The map shows the deployment of US forces as at January 2020. I’ve only crudely updated it to account for US withdrawal from Afghanistan.

Clearly, the conflict between east and west is not over ideology or a bit of territory. It is about hegemony over resource rich regions of the world and this makes the two sides’ positions intractable. The Russians clearly understand this which may explain why they presented the Western powers with a set of demands so tough that they certainly knew they would be rejected. It seems that Russia really does intend to respond with military technical measures that will jeopardize western powers’ security. So far however, even among the Russian analysts, nobody seems to know what’s coming next.

Most of the experts and officials in the West seem convinced that Russia will invade Ukraine, but I don’t think this will happen. The media also made much of Russia’s deputy foreign minister’s remarks that they don’t exclude deploying military assets in Cuba or Venezuela, which can’t be excluded longer term. A few analysts including Scott Ritter suggested that Russians might deploy medium-short range missiles targeting European capitals with nuclear capable warheads.

The Kremlin will probably increase pressure on the US and NATO countries in multiple ways, but my own hunch is that their first focus will be on the Persian Gulf region which is strategically of huge importance to the West but where US positions are increasingly fragile. Russia could jeopardize western power’s security in that region by implementing “military technical measures” in support of friendly regimes, primarily Iran. It is clear that Iran is becoming an important component of China’s One Belt One Road agenda and that it is being set up as the cornerstone of their security architecture in the Middle East and the Persian Gulf. These developments also have the full support from Russia.

On 27 March last year, Iran signed a comprehensive 25-year cooperation plan with China which includes cultural, diplomatic, economic and military cooperation. On 17 September Iran became a member of the Shanghai Cooperation Organization (SCO). Iran has also signed various security agreements with Russia and is in the process of negotiating a 20-year cooperation agreement modeled on the Iran-China agreement.

On 11 December 2021, Iranian foreign ministry spokesman Saeed Khatibzadeh stated that, “Like the 25-year cooperation roadmap we developed with China, we can do the same with major neighboring countries.” Clearly, the Iranians, who have pledged to throw the United States out of the region, have been increasingly confident in asserting their regional influence. Of course, the greatest challenge to Iran’s regional policy and security is the presence of American troops and military bases surrounding Iran as this map shows. The map shows the deployment of US forces as at January 2020. I’ve only crudely updated it to account for US withdrawal from Afghanistan.

Már megemlegették. Most azért szövetkeznek.Britek nem bírnak magukkal, már a lengyelek se. Rendre kéne tanítani mind a kettőt, úgy hogy örökre megemlegetik.

Incidentally, the above map illustrates another reason why the hold on Afghanistan was so important to the empire.

Iran’s partnership with Russia and China will ultimately tip the military balance of power, so it was perhaps no coincidence that Iran’s President Ebrahim Raisi’s visit to Moscow was scheduled for Wednesday, 19 January 2022 – only days after the failed talks between Russia and the US in Geneva. In announcing the meeting, Russian Foreign Minister Sergei Lavrov said it was a “very important” meeting and added that, “Undoubtedly, among international issues, the ones such as the Joint Comprehensive Plan of Action and the security of the Persian Gulf will be discussed in the meeting of the Presidents of Iran and Russia.”

At the opening of his meeting with President Putin, Mr. Raisi said that the relationship between the two nations “should be permanent and strategic.” In his address to the Russian Duma, he said that, “The strategy of domination has now failed, the United States is in its weakest position, and the power of independent nations is experiencing historic growth.” President Raisi’s visit to Moscow was followed two days later by military exercises of Russian, Iranian and Chinese navies in the Sea of Oman, not far from the strategically pivotal Straits of Hormuz. The three powers’ show of force was an unmistakable hint that there’s a new sheriff in town and that the days of unchallenged US/NATO dominance over the region are over.

Thus, the “military technical” measures Russia promised if the US and NATO did not agree to her draft treaties will likely be made in support of forces that are already fighting to drive the western powers out of the region. Iran is obviously the prime candidate for such support and during his visit in Moscow President Raisi did not fail underscore Iran’s credibility and commitment to this objective in stating, “We have been resisting the Americans for 40 years.” Together with its proxy forces in Iraq, Iran will make it increasingly difficult and costly for the US to secure its control of the region.

Russia will not need to confront the US militarily at all – the US forces will simply be worn down and eventually pushed out in a similar way as they were pushed out from Afghanistan. For the Western nations which are already facing a worsening energy crisis, this could indeed jeopardize their security. But it could also have severe adverse effects on their economies and capital markets. Paradoxically however, for that same reason the western powers will not advertise that their control is slipping away; they will likely take their blows in silence and keep a brave face for as long as possible to keep the markets convinced that their revenue streams from the Middle East will remain secure forever.

I first published what I laid out here in my daily TrendCompass newsletter on 14th January, titled “Only a hunch: will it be the Persian Gulf?” I can confess, this really is only a hunch, based on my own reading of the situation. However, as events have played out over the last two weeks, I am increasingly confident that my hunch was correct. At the same time however, I couldn’t begin to guess how exactly the events might play out. For one thing, the uncertainty is probably part of the equation: Russia’s current gambit is very radical departure from the status quo and it should be to her advantage to keep her adversaries guessing and distracted in the wrong places. Indeed, it is possible that nothing obvious will happen over the coming weeks. All the same, we should not underestimate changes that are already taking place. As they compound, they will precipitate a collapse of the global order that has become entrenched for more than two centuries now.

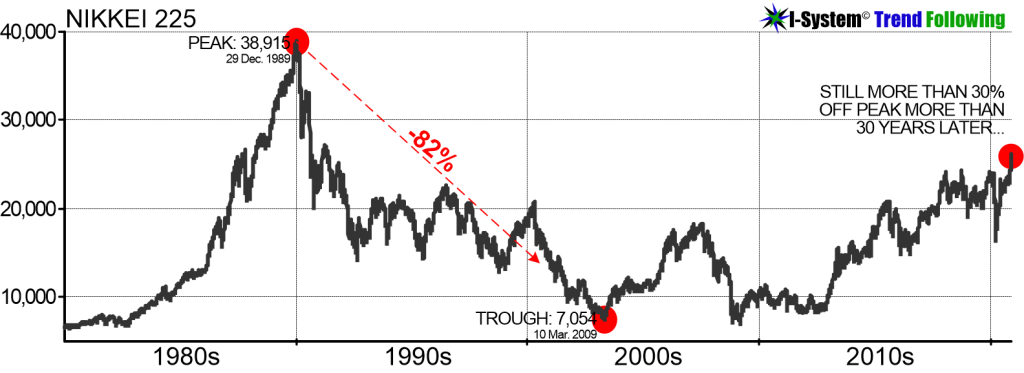

In both cases we saw stock prices decline by over 80%. The US stock market took nearly three decades to fully recover while the Nikkei never recovered, after fully 32 years since the 1989 peak.

We are also likely to see a continued acceleration of inflation in most if not all of the G7 nations, as well as a gradual worsening of the energy crisis which could drag on for years. This could push the energy prices far beyond today’s levels. Even without factoring the conflict with Russia and based on the accelerating depletion of conventional oil reserves, the UK Ministry of Defence predicted in 2012 that the price of Crude Oil would rise to $500/bbl by 2040. Similar trends could materialize in other commodities including metals and agricultural produce, fueling a sustained commodity super-cycle that many analysts have been predicting in the recent years.

Iran’s partnership with Russia and China will ultimately tip the military balance of power, so it was perhaps no coincidence that Iran’s President Ebrahim Raisi’s visit to Moscow was scheduled for Wednesday, 19 January 2022 – only days after the failed talks between Russia and the US in Geneva. In announcing the meeting, Russian Foreign Minister Sergei Lavrov said it was a “very important” meeting and added that, “Undoubtedly, among international issues, the ones such as the Joint Comprehensive Plan of Action and the security of the Persian Gulf will be discussed in the meeting of the Presidents of Iran and Russia.”

At the opening of his meeting with President Putin, Mr. Raisi said that the relationship between the two nations “should be permanent and strategic.” In his address to the Russian Duma, he said that, “The strategy of domination has now failed, the United States is in its weakest position, and the power of independent nations is experiencing historic growth.” President Raisi’s visit to Moscow was followed two days later by military exercises of Russian, Iranian and Chinese navies in the Sea of Oman, not far from the strategically pivotal Straits of Hormuz. The three powers’ show of force was an unmistakable hint that there’s a new sheriff in town and that the days of unchallenged US/NATO dominance over the region are over.

Thus, the “military technical” measures Russia promised if the US and NATO did not agree to her draft treaties will likely be made in support of forces that are already fighting to drive the western powers out of the region. Iran is obviously the prime candidate for such support and during his visit in Moscow President Raisi did not fail underscore Iran’s credibility and commitment to this objective in stating, “We have been resisting the Americans for 40 years.” Together with its proxy forces in Iraq, Iran will make it increasingly difficult and costly for the US to secure its control of the region.

Russia will not need to confront the US militarily at all – the US forces will simply be worn down and eventually pushed out in a similar way as they were pushed out from Afghanistan. For the Western nations which are already facing a worsening energy crisis, this could indeed jeopardize their security. But it could also have severe adverse effects on their economies and capital markets. Paradoxically however, for that same reason the western powers will not advertise that their control is slipping away; they will likely take their blows in silence and keep a brave face for as long as possible to keep the markets convinced that their revenue streams from the Middle East will remain secure forever.

I first published what I laid out here in my daily TrendCompass newsletter on 14th January, titled “Only a hunch: will it be the Persian Gulf?” I can confess, this really is only a hunch, based on my own reading of the situation. However, as events have played out over the last two weeks, I am increasingly confident that my hunch was correct. At the same time however, I couldn’t begin to guess how exactly the events might play out. For one thing, the uncertainty is probably part of the equation: Russia’s current gambit is very radical departure from the status quo and it should be to her advantage to keep her adversaries guessing and distracted in the wrong places. Indeed, it is possible that nothing obvious will happen over the coming weeks. All the same, we should not underestimate changes that are already taking place. As they compound, they will precipitate a collapse of the global order that has become entrenched for more than two centuries now.

How the coming changes will manifest in the West

Russia will probably not invade Ukraine and Russian bombs won’t start raining down on European cities. We’re living in the age of assymetric warfare and it is quite likely that nothing obvious will be captured by TV cameras. But the pain will set in and it will be real. I believe that the changes will be felt most strongly in our capital and commodities markets. Over time, we’ll see a very substantial rise in interest rates which will ultimately push stock prices into a real bear market. Unlike the limited and short-lived corrections we’ve experienced over the last four decades, a real bear market could be drastic and last a very long time. It is what happened in the US after the 1920s bubble and in Japan after the 1980s bubble.

In both cases we saw stock prices decline by over 80%. The US stock market took nearly three decades to fully recover while the Nikkei never recovered, after fully 32 years since the 1989 peak.

We are also likely to see a continued acceleration of inflation in most if not all of the G7 nations, as well as a gradual worsening of the energy crisis which could drag on for years. This could push the energy prices far beyond today’s levels. Even without factoring the conflict with Russia and based on the accelerating depletion of conventional oil reserves, the UK Ministry of Defence predicted in 2012 that the price of Crude Oil would rise to $500/bbl by 2040. Similar trends could materialize in other commodities including metals and agricultural produce, fueling a sustained commodity super-cycle that many analysts have been predicting in the recent years.

17:35-nél mondja, hogy Eu-nak lesznek gondjai gáz téren, de Magyarországnak nem.az 1milliárd plussz gázról áprilisben lesz döntés, vagy nem

")

Amúgy visszatérve a találkozóra, az még érdekes volt, hogy Orbán mintegy Európa nevében kijelentette, hogy senki sem akar háborút Oroszországgal Európából. Mintegy küldött. A többiek nem mertek odamenni... Ilyen az amikor elszigetelve vagyunk s senki sem vesz minket komolyan (bár nem szeretnék semmilyen belpolt indítani ezzel, csak úgy feltört belőlem...)

A nyugati puhányok, akik nem falun meg kollégiumi menzán nőttek fel, nem bírják a polóniumos teát.Amúgy visszatérve a találkozóra, az még érdekes volt, hogy Orbán mintegy Európa nevében kijelentette, hogy senki sem akar háborút Oroszországgal Európából. Mintegy küldött. A többiek nem mertek odamenni... Ilyen az amikor elszigetelve vagyunk s senki sem vesz minket komolyan (bár nem szeretnék semmilyen belpolt indítani ezzel, csak úgy feltört belőlem...)

14:08-nál.Az orosz - magyar vegyesvállalat megvolt? Orbán: "a határainkon.. az ukrán - magyar határon" véletlen elszólás

Orbán fészbúkos élőjében 14:05 után.Erről sajnos lemaradtam

Az ukránoknak is úgy néz ki lesz, vesznek a lengyelektől LNG-t, ami gondolom amerikai vagy "amerikai". Biztos jó olcsó lesz...17:35-nél mondja, hogy Eu-nak lesznek gondjai gáz téren, de Magyarországnak nem.

Polonia anunță că va furniza Ucrainei gaz natural lichefiat și promite un nou ajutor de arme defensive, în cazul unei invazii lansate de Rusia. - Biziday

“Trăind atât de aproape de un vecin precum Rusia, avem senzația că ne aflăm la poalele unui vulcan”, a declarat premierul polonez Mateusz Morawiecki, care

www.biziday.ro

www.biziday.ro

Én is ezt vettem le, mint ha az EU szabad kezet adott volna Putyinnak és egyezkedésre hívta.Amúgy visszatérve a találkozóra, az még érdekes volt, hogy Orbán mintegy Európa nevében kijelentette, hogy senki sem akar háborút Oroszországgal Európából. Mintegy küldött. A többiek nem mertek odamenni... Ilyen az amikor elszigetelve vagyunk s senki sem vesz minket komolyan (bár nem szeretnék semmilyen belpolt indítani ezzel, csak úgy feltört belőlem...)

"Európai Unió részéről készen állunk egy ésszerű megállapodásra, az EU egyetlen vezetője sem akar háborút."

Aztán, 5 óra zárt ajtók mögött. Komoly dolgokról lehetett szó, nem hiszem, hogy a +2 Aeroflot járatról beszélgettek ilyen sokat.